Table of Contents

Dubai’s real estate market has always been driven by its facilities. When a city opens a new mobility link or adds a high-capacity transit

How Dubai New Infrastructure Projects Are Driving Property Value route, it changes where people live, how they get to work, and how much they’re willing to pay. Today, three groups are working together to change the prices in whole districts:

1. The growth of the Dubai Metro, especially the new Blue Line.

2. Major road improvements that clear up important east-west and north-south routes.

3. The Dubai 2040 Urban Master Plan, which focuses growth on linked, mixed-use hubs.

This in-depth look explains why and where prices are changing, turning choices about transportation and planning into information that investors can use.

The Dubai New Infrastructure Projects: How Transport Creates Property Value

Investing Dubai New Infrastructure Projects starts a simple but strong chain reaction:

- It takes less time to get from door to door and there are more jobs, schools, and services nearby.

- Tenants and buyers change the order of neighbourhoods based on how easy they are to live in (time saved) and how reliable they are (multiple paths).

- Density and amenities improve: stores and services open up around stops and interchanges, and developers bring in higher-quality stock.

- Pricing power: Lower transportation costs and a wider range of amenities support higher rents and property values.

- Reinforcement: Public and private capital flow along successful routes, keeping them performing better.

This is especially clear in Dubai near metro stations and newly cleared-out intersections: “micro-markets” that are close enough to walk to appear within 800–1,200 metres of stations and at better interchanges, and they take in a huge chunk of demand growth.

The Dubai Metro Effect: What the Data Already Shows

There is a lot of proof that shows how valuable it is to be close to metro stations in Dubai:

- According to a peer-reviewed hedonic pricing study, residential properties located about 700 to 900 metres from new stations saw a big increase in value, and business properties saw even bigger increases after the stations opened.

- According to the CBRE Dubai Metro Report 2023, homes within a 15-minute walk of Red Line stops did better than the rest of the market. Prices rose 26.7% from 2010 to 2022 compared to 24.1% across the city, and rentals also did better than the average for the city. It’s interesting that prices rose the most in the 10–15 minute band, which suggests that a movable “walkshed” goes beyond the front door.

Investors should know this: being close to a station is important, but you don’t have to be on top of the platform. Having property 600–1,200 m from a metro station can give you a price advantage and real “metro utility,” especially if the walking paths are clear and well-lit.

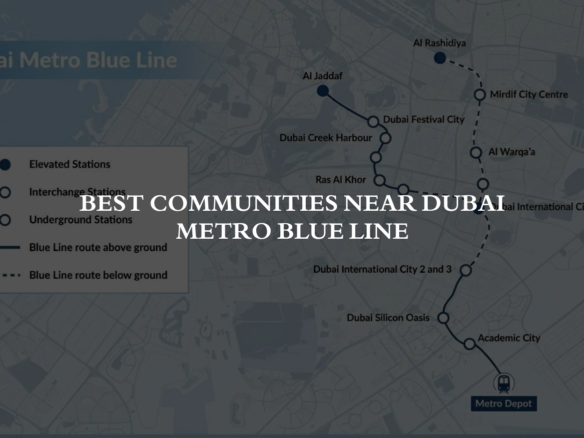

Blue Line: The Next Big Repricing

The 30 km, 14-station Dubai Metro Blue Line is the city’s most important transportation investment this cycle. It will connect to the Green Line at Creek and the Red Line at Centerpoint, and it’s set to open in 2029. In December 2024, RTA gave a MAPA–Limak–CRRC consortium a construction contract worth AED 20.5 billion (~$5.6 billion). This was a big step that made the program’s delivery less risky. You can expect the line to connect Academic City, Dubai Silicon Oasis, Dubai Creek Harbour, Ras Al Khor, Mirdif, and Al Warqaa. It will end at a depot in Al Ruwayyah 3.

The places where prices are most likely to change first-

Before pricing (when there is more certainty) and after opening (when time savings are realized), infrastructure-led appreciation is more likely to happen. Keep an eye on these small stores along the Blue Line:

Dubai Creek Harbour (DCH) is a famous waterfront area that will be anchored by a future interchange and a famous station. As the edge of the CBD with major master-developer oversight, DCH is set up for both rental stability (because it’s easy to get to Downtown and Business Bay via interchanges) and capital gains once the line opens. You can expect premiums to rise near the station and along direct pedestrian spines.

Corridors between Ras al Khor and Al Warqaa

Historically reliant on cars, these areas will change latent demand once rapid transit is up and running. Increasing access and increasing land use (mid-rise/mixed-use near stations) are common ways to create value here. This is a classic example of transit-oriented development (TOD).

“International City” (Phase 1 and more)

When you have a lot of tenants and they are price conscious, time savings translate strongly into rent. It’s possible for yields to rise before capital values do again, especially for stocks that are only a 10–15 minute walk from International City 1, which is where Blue branches connect.

Academic City and Dubai Silicon Oasis (DSO)

People who are students or work in knowledge are very sensitive to transit. You can expect people to mostly buy projects that are close to train stations, and developers will respond by building mixed-use plots with co-living, student housing, and serviced apartments.

Red & Green Lines: Mature Lines, Persistent Premiums

- The “proximity dividend” can still be seen: CBRE data shows that prices and rents have done better over the long term near the Red Line. The compounding effect can be seen in places like Dubai Marina, JLT, Business Bay, and Downtown. These areas have lots of jobs and good rail connections, which keeps vacancies low and raises blended yields.

- On the Green Line, places like Deira, Al Qusais, and Bur Dubai have benefited from network effects, which means that older buildings and bus interchanges have become easier for people to get to. This has helped value investors get steady rent-based returns.

Road Expansions: Where Driving Still Decides the Rent

While rail shapes dense urban cores, road capacity and junction design still determine Even though rail shapes dense urban cores, road capacity and junction design still decide where people can live and how much they are worth in villa districts and apartment communities that are geared toward cars. Two improvements affect the whole city:

Project to Make Hessa Street Better

The multi-phase upgrade adds about 9 km of bridges and about 13.5 km of parallel roads. It also redesigns major intersections like Sheikh Zayed Road, Al Khail Road, and First Al Khail Street. The goal is to double the number of vehicles that can pass through each hour, from about 4,000 to about 8,000. All intersections should be fully operational by the fourth quarter of 2025. This directly lowers last-mile friction for communities that cross Hessa, like JVC, JVT, Dubai Sports City, Al Barsha, and the Al Hebiah corridor. This makes more people want to live there.

Corridor of Al Shindagha

A program that has been going on for a long time that lets people flow smoothly from Al Garhoud Bridge to Infinity Bridge. When the last bridge on the Bur Dubai side opens in May 2025, it will be easier for people to get across the Creek in historic areas of Deira and Bur Dubai. This will help stores stay open and increase demand for homes.

Why it’s important: Even in places with lots of public transportation, having good roads and rail adds to the number of potential tenants. A neighborhood that works for people who take the train or car to get to work will be able to handle shocks better and get a higher price.

Dubai 2040 Urban Master Plan: The Policy Backstop

Infrastructure isn’t just there; it’s put in place by planning. The Dubai 2040 Urban Master Plan is the set of policies that will direct growth to places where there will be enough space for transportation. Some important pillars are:

- “20-minute city”-style growth that is compact and mixed-use: In model districts, 80% of daily needs can be met with a short walk or ride on public transportation.

- Green and leisure areas were doubled, making public spaces healthier and easier to walk through.

- Mobility shift: putting high-capacity transit and active mobility first, and making station areas busier.

As a result of 2040 planning documents & Dubai New Infrastructure Projects, areas that are marked for more people living in close quarters and better public transportation tend to see earlier private investment and faster permit cycles, which are both good for buyers and developers.

Neighborhood-by-Neighborhood: Who Benefits Most (and How)

1) Dubai Creek Harbour (DCH) & Ras Al Khor

- Catalyst: Blue Line interchange + landmark station; improved east-west road Blue Line interchange and landmark station, as well as better east-west road connections, will act as a catalyst.

- Demand: People want to live near the CBD without having to pay Downtown prices, live on the water, and use rapid transit to get to and from work.

- Thesis: Early-cycle repricing as execution risk goes down; after the opening, the premium grows for towers that are directly connected to the station by footpaths.

2) International City & Warsan

- Catalyst: connecting the Blue Line and adding an interchange; integrating buses and trains more.

- Demand: Value-driven tenants, high rents, and jobs in the service sector are what drive demand.

- Thesis: First there is rent compression (vacancy down), then capital values rise as landlords get consistently higher effective rents.

3) Dubai Silicon Oasis (DSO) & Academic City

- Catalyst: Growth of the Blue Line, student, and tech clusters.

- Demand: Education hubs, professionals who are cost-conscious, and the desire for furnished, managed stock are the things that drive demand.

- Thesis: The transit and student pipeline helps unique housing types (like co-living and student housing) and steady rent growth.

4) JVC, JVT, and the Hessa Corridor

- Catalyst: make improvements to Hessa Street and the intersections at SZR, Al Khail, and First Al Khail.

- Demand: Families are willing to trade more space for a more reliable commute, and prices are being found as traffic jams get better.

- Thesis: Car-dependent areas re-rate when commutes become less unpredictable. Look for townhouses and mid-rise buildings that are close to better interchanges.

5) Bur Dubai & Deira (Historic Core)

- Catalyst: Finishing the Al Shindagha Corridor and connecting multiple bridges.

- Demand: SMEs and retail, tourism, and residents who use both buses and cars are the main drivers of demand.

- Thesis: Reliability, not just speed, makes people more likely to want to live and shop across the Creek. Expect rents to rise slowly but steadily and shop occupancy to improve.

Investor Playbook: Turning Transit and Road Maps into Returns

Cover the “effective” walkshed, not just the straight-line distance.

Use real paths for people. A 10–15 minute walk in the shade is safer than a 5–8 minute walk across dangerous roads. The results that CBRE found in the 10–15 minute band back up this nuance.

Buy now, before the price of certainty goes up too much.

Contract awards, visible site work, and major bridge openings are all important signs that the risk has been reduced. The Blue Line contract award in December 2024 was a turning point in this way; prices tend to go up after that.

Choose buildings that can be used in two different ways.

If a property is close enough to a subway station to walk to and not too far from a major road, it will attract more tenants and keep the vacancy rate stable.

Pay attention to rentability first, then capital gains.

In high-value areas like International City and DSO, the rent signal usually comes first. This means that you can expect less vacancy, then higher rents, and finally a higher PSF sale price.

Not city averages, but comps from small markets.

Bayut, Dubsizzle, and institutional research all give rental and price indices for specific neighborhoods. These can be used to compare properties to similar ones close to stations instead of using district medians as a whole.

Test deadlines under stress.

Things like rail lines and road work can move. Imagine that the benefits don’t show up for 12 to 18 months as planned, and make sure that your yield still works while construction is going on (noise, traffic changes).

Developer & Landlord Strategies That Capture the Premium

Plan for the “last 500 meters.”

Safe access points for pedestrians, shaded arcades, and micro-mobility parking (for e-scooters and bikes). This makes an okay walk into a nice one key for the 10–15 minute ring

Choosing the right amenities for stations.

Ground-floor stores that fit the habits of commuters like grab-and-go food, convenience stores, and package lockers have higher rates of new tenants and renewals.

Flexible unit mixes in hallways for students and tech workers.

To get the most out of your NOI, plan more studios and 1-beds with study rooms and co-working lounges in DSO/Academic City. In International City, focus on practical layouts and long-lasting finishes.

Plan for parking at road-led micromarkets.

Until rail arrives, features like slightly higher parking ratios and easy access to better intersections along Hessa and in areas with lots of villas can be used to make money.

Risks & Reality Checks

Temporary noise, dust, and other distractions caused by construction can turn away potential tenants. Talk about allowances for assets that are still being built and set up leasing accordingly.

Cycles of speculation: Early hype can go too far. Follow the rules for cash flow and aim for above-trend yields while you wait for the mobility dividend to show up.

Policy and phasing risk: The actual value captured will depend on how far apart stations are, how well buses are integrated, and how good the pedestrian realm is. Do not just look at the marketing maps; also read the Dubai Municipality’s 2040 implementation notes and RTA design updates.

What to Watch (2025–2029)

Blue Line construction milestones, such as the start of tunneling, station structural work, and system integration, that usually happen 12 to 24 months before pre-opening prices become firm.

If Hessa Street is fully operational by the fourth quarter of 2025 and traffic data is collected after it opens, leasing will pick up in the next two to three quarters.

More improvements to the Al Shindagha Corridor (signal timing, feeder bus patterns) will make cross-Creek trips and retail foot traffic better.

Changes at the district level in the 2040 Plan include rezoning, improvements to the public realm, and model “20-minute city” pilots that are bigger than Al Barsha 2 prototypes. These allow for more density and mixed-use value.

Need a More information About It?

Our agents will help you explore premium options tailored to your lifestyle, location preferences, and investment goals.

Conclusion

The next part of Dubai New Infrastructure Projects will be concentrated where rail meets roads, where there is a clear vision for land use. The Blue Line is the main thing that connects affordable hubs and knowledge-economy districts. The Hessa Street and Al Shindagha upgrades make it safer for families to drive to work, and the Dubai 2040 Urban Master Plan keeps everything pointing toward walkable, mixed-use centers that are served by transit.

The game plan for buyers and developers is always the same: own the last-mile experience (to stations and better junctions), buy the de-risking, and price like an operator (yields first, appreciation second). In a market like Dubai, where infrastructure is very important, maps are more than just directions.

FAQs

They make it easier to get around, add services, and raise demand, which raises both rental rates and resale prices.

It includes the Blue Line of the Dubai Metro, the revitalization of Palm Jebel Ali, and major road improvements like the Sheikh Zayed Corridor.

Yes. Properties close to new metro stops usually go up in value because they are easier to get to.

Of course. Zones close to new airports, shops, and roads get more investors and see their money grow faster.

Yes. The Dubai 2040 Urban Master Plan calls for ongoing growth, which is likely to keep driving up property costs.

Join The Discussion